Bollinger Breakout Strategy with Direction Control [4H crypto]Bollinger Breakout Strategy with Direction Control - User Guide

This strategy leverages Bollinger Bands, RSI, and directional filters to identify potential breakout trading opportunities. It is designed for traders looking to capitalize on significant price movements while maintaining control over trade direction (long, short, or both). Here’s how to use this strategy effectively:

How the Strategy Works

Indicators Used:

Bollinger Bands:

A volatility-based indicator with an upper and lower band around a simple moving average (SMA). The bands expand or contract based on market volatility.

RSI (Relative Strength Index):

Measures momentum to determine overbought or oversold conditions. In this strategy, RSI is used to confirm breakout strength.

Trade Direction Control:

You can select whether to trade:

Long only: Buy positions.

Short only: Sell positions.

Both: Trade in both directions depending on conditions.

Breakout Conditions:

Long Trade:

The price closes above the upper Bollinger Band.

RSI is above the midline (50), confirming upward momentum.

The "Trade Direction" setting allows either "Long" or "Both."

Short Trade:

The price closes below the lower Bollinger Band.

RSI is below the midline (50), confirming downward momentum.

The "Trade Direction" setting allows either "Short" or "Both."

Risk Management:

Stop-Loss:

Long trades: Set at 2% below the entry price.

Short trades: Set at 2% above the entry price.

Take-Profit:

Calculated using a Risk/Reward Ratio (default is 2:1).

Adjust this in the strategy settings.

Inputs and Customization

Key Parameters:

Bollinger Bands Length: Default is 20. Adjust based on the desired sensitivity.

Multiplier: Default is 2.0. Higher values widen the bands; lower values narrow them.

RSI Length: Default is 14, which is standard for RSI.

Risk/Reward Ratio: Default is 2.0. Increase for more aggressive profit targets, decrease for conservative exits.

Trade Direction:

Options: "Long," "Short," or "Both."

Example: Set to "Long" in a bullish market to focus only on buy trades.

How to Use This Strategy

Adding the Strategy:

Paste the script into TradingView’s Pine Editor and add it to your chart.

Setting Parameters:

Adjust the Bollinger Band settings, RSI, and Risk/Reward Ratio to fit the asset and timeframe you're trading.

Analyzing Signals:

Green line (Upper Band): Signals breakout potential for long trades.

Red line (Lower Band): Signals breakout potential for short trades.

Blue line (Basis): Central Bollinger Band (SMA), helpful for understanding price trends.

Testing the Strategy:

Use the Strategy Tester in TradingView to backtest performance on your chosen asset and timeframe.

Optimizing for Assets:

Forex pairs, cryptocurrencies (like BTC), or stocks with high volatility are ideal for this strategy.

Works best on higher timeframes like 4H or Daily.

Best Practices

Combine with Volume: Confirm breakouts with increased volume for higher reliability.

Avoid Sideways Markets: Use additional trend filters (like ADX) to avoid trades in low-volatility conditions.

Optimize Parameters: Regularly adjust the Bollinger Bands multiplier and RSI settings to match the asset's behavior.

By utilizing this strategy, you can effectively trade breakouts while maintaining flexibility in trade direction. Adjust the parameters to match your trading style and market conditions for optimal results!

Cerca negli script per "the script"

TFMTFM Strategy Explanation

Overview

The TFM (Timeframe Multiplier) strategy is a PineScript trading bot that utilizes multiple timeframes to identify entry and exit points.

Inputs

1. tfm (Timeframe Multiplier): Multiplies the chart's timeframe to create a higher timeframe for analysis.

2. lns (Long and Short): Enables or disables short positions.

Logic

Calculations

1. chartTf: Gets the chart's timeframe in seconds.

2. tfTimes: Calculates the higher timeframe by multiplying chartTf with tfm.

3. MintickerClose and MaxtickerClose: Retrieve the minimum and maximum closing prices from the higher timeframe using request.security.

- MintickerClose: Finds the lowest low when the higher timeframe's close is below its open.

- MaxtickerClose: Finds the highest high when the higher timeframe's close is above its open.

Entries and Exits

1. Long Entry: When the current close price crosses above MaxtickerClose.

2. Short Entry (if lns is true): When the current close price crosses below MintickerClose.

3. Exit Long: When the short condition is met (if lns is false) or when the trade is manually closed.

Strategy

1. Attach the script to a chart.

2. Adjust tfm and lns inputs.

3. Monitor entries and exits.

Example Use Cases

1. Intraday trading with tfm = 2-5.

2. Swing trading with tfm = 10-30.

Tips

1. Experiment with different tfm values.

2. Use lns to control short positions.

3. Combine with other indicators for confirmation.

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

Monday Open StrategyYear Range Inputs:

start_year and end_year allow you to define the range of years in which the strategy will execute.

You can adjust these values in the script’s settings panel in TradingView.

Entry Condition:

The strategy checks that the current year falls within the specified range before entering a trade on Monday’s open.

Exit Condition:

Similarly, it only exits on Tuesday’s close if the current year is within the specified range.

This setup ensures that trades only take place between the defined years, effectively filtering out unwanted trades outside this timeframe.

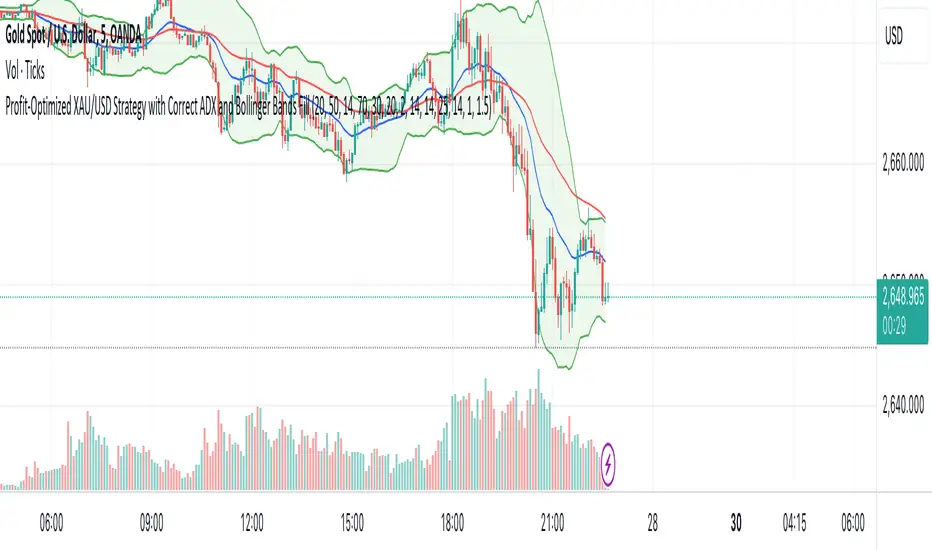

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

All Divergences with trend / SL - Uncle SamThanks to the main inspiration behind this strategy and the hard work of:

"Divergence for many indicators v4 by LonesomeTheBlue"

The "All Divergence" strategy is a versatile approach for identifying and acting upon various divergences in the market. Divergences occur when price and an indicator move in opposite directions, often signaling potential reversals. This strategy incorporates both regular and hidden divergences across multiple indicators (MACD, Stochastics, CCI, etc.) for a comprehensive analysis.

Key Features:

Comprehensive Divergence Analysis: The strategy scans for regular and hidden divergences across a variety of indicators, increasing the probability of identifying potential trade setups.

Trend Filter: To enhance accuracy, a moving average (MA) trend filter is integrated. This ensures trades align with the overall market trend, reducing the risk of false signals.

Customizable Risk Management: Users can adjust parameters for long/short stop-loss and take-profit levels to match their individual risk tolerance.

Additional Risk Management (Optional): An experimental MA-based risk management feature can be enabled to close positions if the market shows consecutive closes against the trend.

Clear Visuals: The script plots pivot points, divergence lines, and stop-loss levels on the chart for easy reference.

Strategy Settings (Defaults):

Enable Long/Short Strategy: True

Long/Short Stop Loss %: 2%

Long/Short Take Profit %: 5%

Enable MA Trend: True

MA Type: HMA (Hull Moving Average)

MA Length: 500

Use MA Risk Management: False (Experimental)

MA Risk Exit Candles: 2 (If enabled)

Pivot Period: 9

Source for Pivot Points: Close

Backtest Details (Example):

The strategy has been backtested on XAUUSD 1H (Goold/USD 1 hour timeframe) with a starting capital of $1,000. The backtest period covers around 2 years. A commission of 0.02% per trade and a 0.1% slippage per trade were factored in to simulate real-world trading costs.

Disclaimer:

This strategy is for educational and informational purposes only. Backtested results are not indicative of future performance. Use this strategy at your own risk. Always conduct your own analysis and consider consulting a financial professional before making any trading decisions.

Important Notes:

The default settings are a good starting point, but feel free to experiment to find optimal parameters for your specific trading style and market.

The MA-based risk management is an experimental feature. Use it with caution and thoroughly test it before deploying in live trading.

Backtest results can vary depending on the market, timeframe, and specific settings used. Always consider slippage and commission fees when evaluating a strategy's potential profitability.

Uptrick:Intensity IndexPurpose:

The "Uptrick: Intensity Index" strategy is designed to provide traders with insights into the trend intensity of security by combining multiple moving averages and their relative positions. This versatile tool can be used effectively by both short-term and long-term traders to identify potential buy and sell signals based on specific conditions.

Explanation:

Input Parameters and Customization:

Moving Averages Lengths:

Adjust MA1, MA2, and MA3 lengths to change the calculation periods for the moving averages.

Trend Intensity Index SMA Length:

Adjust the length of the SMA applied to the TII.

Plot Colors:

Change the colors of the TII and TII MA plots for better visualization.

Background Colors and Transparency:

Set different colors for positive and negative TII MA values.

Control the transparency of the background color.

---------------------------------------------------------------------------

MA1 (Length 10): Short-term moving average, useful for capturing short-term market trends.

MA2 (Length 20): Medium-term moving average, providing a balanced view of market trends.

MA3 (Length 50): Long-term moving average, offering insights into long-term market trends.

The script calculates the relative positions of the closing price to each moving average (rel1, rel2, rel3) to determine how far the current price deviates from each average.

Trend Intensity Index (TII):

The TII is calculated as the average of the relative positions (rel1, rel2, rel3), multiplied by 100 to convert it into a percentage. This index reflects the overall intensity of the trend, considering short-term, medium-term, and long-term perspectives.

The TII is plotted in blue, providing a visual representation of trend intensity.

SMA of TII:

An additional SMA is applied to the TII (matii) to smooth out fluctuations and provide a clearer long-term trend signal.

The SMA of TII is plotted in orange, offering a reference for long-term trend analysis.

Determining Potential Price Movements:

For Short-Term Traders:

When the blue TII line crosses above the orange SMA of TII line, it indicates a potential buy signal.

When the blue TII line crosses below the orange SMA of TII line, it indicates a potential sell signal.

For Long-Term Traders:

When the orange SMA of TII line crosses above the highlighted 0 line, it indicates a potential buy signal.

When the orange SMA of TII line crosses below the highlighted 0 line, it indicates a potential sell signal.

Plotting and Visualization:

The TII and its SMA are plotted with distinct colors for easy identification.

A horizontal line at 0 is plotted in gray to serve as a reference point for long-term trend signals.

The background color changes based on the value of the SMA of TII (matii):

Green background for matii values above 0, indicating bullish conditions.

Red background for matii values below 0, indicating bearish conditions.

Utility and Potential Usage:

The "Uptrick: Intensity Index" indicator is a powerful tool for both short-term and long-term traders, offering clear buy and sell signals based on the crossover of the TII and its SMA, as well as the position of the SMA relative to the zero line.

By consolidating multiple moving averages and their relative positions into a single indicator, traders can gain comprehensive insights into market trends and intensity.

The ability to adjust all inputs and toggle visibility options enhances the flexibility and utility of the indicator, making it suitable for various trading styles and market conditions.

Through its versatile design and advanced features, the "Uptrick: Intensity Index" indicator equips traders with actionable insights into trend intensity and potential price movements. By integrating this robust tool into their trading strategies, traders can navigate the markets with greater precision and confidence, thereby enhancing their trading outcomes.

WHAT SETTINGS TO HAVE FOR THE MOVING AVERAGE:

Short-term traders (day traders) might prefer a shorter SMA length (e.g., 5-20 periods) as they are looking for quick signals and react to price changes more rapidly.

Medium-term traders (swing traders) might opt for a medium SMA length (e.g., 20-50 periods) which can filter out some noise and provide a clearer signal on the trend.

Long-term traders (position traders) might choose a longer SMA length (e.g., 50-200 periods) to get a broader view of the market trend and avoid reacting to short-term fluctuations.

Momentum Alligator 4h Bitcoin StrategyOverview

The Momentum Alligator 4h Bitcoin Strategy is a trend-following trading system that operates on dual time frames. It utilizes the 1D Williams Alligator indicator to identify the prevailing major price trend and seeks trading opportunities on the 4-hour (4h) time frame when the momentum is turning up. The strategy is designed to close trades if the trend fails to develop or holding position if price continues increasing without any significant correction. Note that this strategy is specifically tailored for the 4-hour time frame.

Unique Features

2-layers market noise filtering system: Trades are only initiated in the direction of the 1D trend, determined by the Williams Alligator indicator. This higher time frame confirmation filters out minor trade signals, focusing on more substantial opportunities. At the same time, strategy has additional filter on 4h time frame with Awesome Oscillator which is showing the current price momentum.

Flexible Risk Management: The strategy exclusively opens long positions, resulting in fewer trades during bear markets. It incorporates a dynamic stop-loss mechanism, which can either follow the jaw line of the 4h Alligator or a user-defined fixed stop-loss. This flexibility helps manage risk and avoid non-trending markets.

Methodology

The strategy initiates a long position when the d-line of Stochastic RSI crosses up it's k-line. It means that there is a high probability that price momentum reversed from down to up. To avoid overtrading in potentially choppy markets, it skips the next two trades following a winning trade, anticipating sideways movement after a significant price surge.

This strategy has two layers trades filtering system: 4h and 1D time frames. The first one is awesome oscillator. It shall be increasing and value has to be higher than it's 5-period SMA. This is an additional confirmation that long trade is opened in the direction of the current momentum. As it was mentioned above, all entry signals are validated against the 1D Williams Alligator indicator. A trade is only opened if the price is above all three lines of the 1D Alligator, ensuring alignment with the major trend.

A trade is closed if the price hits the 4h jaw line of the Alligator or reaches the user-defined stop-loss level.

Risk Management

The strategy employs a combined approach to risk management:

It allows positions to ride the trend as long as the price continues to move favorably, aiming to capture significant price movements. It features a user-defined stop-loss parameter to mitigate risks based on individual risk tolerance. By default, this stop-loss is set to a 2% drop from the entry point, but it can be adjusted according to the trader's preferences.

Justification of Methodology

This strategy leverages Stochastic RSI on 4h time frame to open long trade when momentum started reversing to the upside. On the one hand, Stochastic RSI is one of the most sensitive indicator, which allows to react fast on the potential trend reversal. On the other hand, this indicator can be too sensitive and provide a lot of false trend changing signals. To eliminate this weakness we use two-layers trades filtering system.

The first layer is the 4h Awesome oscillator. This is less sensitive momentum indicator. Usually it starts increasing when price has already passed significant distance from the actual reversal point. The strategy opens long trade only is Awesome oscillator is increasing and above it's 5-period SMA. This approach increases the probability to filter the false signals during the choppy market or if the reversal is false.

The second layer filter is the Williams Alligator indicator on 1D time frame. The 1D Alligator serves as a filter for identifying the primary trend and increases probability to avoid the trades with low potential because trading against major trend usually is more risky. It's much better to catch the trend continuation than local bounce.

Last but not least feature of this strategy is close trades condition. It uses the flexible approach. First of all, user can set up the fixed stop-loss according to his own risk-tolerance, by default this value is 2% of price movement. It restricts the potential loss at the moment when trade has just been opened. Moreover strategy utilizes the 4h Williams Alligator's jaw line to exit the trade. If price fell below it trade is closed. This approach helps to not keep open trade if trend is not developing and hold it if price continues going up.

Backtest Results:

Operating window: Date range of backtests is 2021.01.01 - 2024.05.01. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Initial capital: 10000 USDT

Percent of capital used in every trade: 50%

Maximum Single Position Loss: -3.04%

Maximum Single Profit: +29.67%

Net Profit: +6228.01 USDT (+62.28%)

Total Trades: 118 (24.58% win rate)

Profit Factor: 1.71

Maximum Accumulated Loss: 1527.69 USDT (-11.52%)

Average Profit per Trade: 52.78 USDT (+0.89%)

Average Trade Duration: 60 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters.

How to Use:

Add the script to favorites for easy access.

Apply to the 4h timeframe desired chart (optimal performance observed on the BTC/USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

OBVious MA Strategy [1000X Trader]Exploring OBV: The OBVious MA Strategy

Are you using On Balance Volume (OBV) effectively? OBV is a gift to traders. OBV often provides a leading signal at the outset of a trend, when compression in the markets produces a surge in OBV prior to increased volatility.

This strategy demonstrates one method of utilizing OBV to your advantage. I call it the "OBVious MA Strategy ” only because it is so simple in its mechanics. This is meant to be a demonstration, not a strategy to utilize in live trading, as the primary utility of the OBVious MA indicator is as a volume confirmation filter that complements other components of a strategy. That said, I felt useful to present this indicator in isolation in this strategy to demonstrate the power it holds.

Strategy Features:

• OBV is the core signal: this strategy revolves around the On Balance Volume indicator. OBV is a straightforward indicator: it registers a value by adding total volume traded on up candles, and subtracts total volume on down candles, generating a line by connecting those values. OBV was described in 1963 by Joe Granville in his book "Granville's New Key to Stock Market Profits” in which the author argues that OBV is the most vital key to success as a trader, as volume changes are a major predictor of price changes.

• Dual Moving Averages: here we use separate moving averages for entries and exits. This allows for more granular trade management; for example, one can either extend the length of the exit MA to hold positions longer, or shorten the MA for swifter exits, independently of the entry signals.

Execution: long trades are taken when the OBV line crosses above the Long Entry Moving Average of the OBV. Long exits occur when the OBV line crosses under the Long Exit MA of the OBV. Shorts enter on a cross below the Short Entry MA, and exit on a cross above the Short Exit MA.

• Directional Trading: a direction filter can be set to "long" or "short," but not “both”, given that there is no trend filter in this strategy. When used in a bi-directional strategy with a trend filter, we add “both” to the script as a third option.

Application:

While this strategy outlines entry and exit conditions based on OBV crossovers with designated moving averages, is is, as stated, best used in conjunction with a supporting cast of confirmatory indicators (feel free to drop me a note and tell me how you've used it). It can be used to confirm entries, or you might try using it as a sole exit indicator in a strategy.

Visualization:

The strategy includes conditional plotting of the OBV MAs, which plot based on the selected trading direction. This visualization aids in understanding how OBV interacts with the set moving averages.

Further Discussion:

We all know the importance of volume; this strategy demonstrates one simple yet effective method of incorporating the OBV for volume analysis. The OBV indicator can be used in many ways - for example, we can monitor OBV trend line breaks, look for divergences, or as we do here, watch for breaks of the moving average.

Despite its simplicity, I'm unaware of any previously published cases of this method. The concept of applying MAs or EMAs to volume-based indicators like OBV is not uncommon in technical analysis, so I expect that work like this has been done before. If you know of other similar indicators or strategies, please mention in the comments.

One comparable strategy that uses EMAs of the OBV is QuantNomad’s "On Balance Volume Oscillator Strategy ", which uses a pair of EMAs on a normalized-range OBV-based oscillator. In that strategy, however, entries and exits occur on one EMA crossing the other, which places trades at distinctly different times than crossings of the OBV itself. Both are valid approaches with strength in simplicity.

Yeong RRGThe code outlines a trading strategy that leverages Relative Strength (RS) and Rate of Change (RoC) to make trading decisions. Here's a detailed breakdown of the tactic described by the code:

Ticker and Period Selection: The strategy begins by selecting a stock ticker symbol and defining a period (len) for the calculations, which defaults to 14 but can be adjusted by the user.

Stock and Index Data Retrieval: It fetches the closing price (stock_close) of the chosen stock and calculates its 25-period exponential moving average (stock_ema). Additionally, it retrieves the closing price of the S&P 500 Index (index_close), used as a benchmark for calculating Relative Strength.

Relative Strength Calculation: The Relative Strength (rs) is computed by dividing the stock's closing price by the index's closing price, then multiplying by 100 to scale the result. This metric is used to assess the stock's performance relative to the broader market.

Moving RS Ratio and Rate of Change: The strategy calculates a Simple Moving Average (sma) of the RS over the specified period to get the RS Ratio (rs_ratio). It then computes the Rate of Change (roc) of this RS Ratio over the same period to get the RM Ratio (rm_ratio).

Normalization: The RS Ratio and RM Ratio are normalized using a formula that adjusts their values based on the mean and standard deviation of their respective series over the specified window. This normalization process helps in standardizing the indicators, making them easier to interpret and compare.

Indicator Plotting: The normalized RS Ratio (jdk_rs_ratio) and RM Ratio (jdk_rm_ratio) are plotted on the chart with different colors for visual analysis. A horizontal line (hline) at 100 serves as a reference point, indicating a neutral level for the indicators.

State Color Logic: The script includes a logic to determine the state color (statecolor) based on the previous state color and the current values of jdk_rs_ratio and jdk_rm_ratio. This color coding is intended to visually represent different market states: green for bullish, red for bearish, yellow for hold, and blue for watch conditions.

Signal Generation: The strategy generates buy, sell, hold, and watch signals based on the state color and the indicators' values relative to 100. For example, a buy signal is generated when both jdk_rs_ratio and jdk_rm_ratio are above 100, and the background color is set to green to reflect this bullish condition.

Trade Execution: Finally, the strategy executes trades based on the generated signals. A "BUY" trade is entered when a buy signal is present, and it is closed when a sell signal occurs.

Overall, the strategy uses a combination of RS and RoC indicators, normalized for better comparison, to identify potential buy and sell opportunities based on the stock's performance relative to the market and its momentum.

DCA StrategyIntroducing the DCA Strategy, a powerful tool for identifying long entry and exit opportunities in uptrending assets like cryptocurrencies, stocks, and gold. This strategy leverages the Heikin Ashi candlestick pattern and the RSI indicator to navigate potential price swings.

Core Functionality:

Buy Signal : A buy signal is generated when a bullish (green) Heikin Ashi candle appears after a bearish (red) one, indicating a potential reversal in a downtrend. Additionally, the RSI must be below a user-defined threshold (default: 85) to prevent buying overbought assets.

Sell Signal : The strategy exits the trade when the RSI surpasses the user-defined exit level (default: 85), suggesting the asset might be overbought.

Backtesting Flexibility : Users can customize the backtesting period by specifying the start and end years.

Key Advantages:

Trend-Following: Designed specifically for uptrending assets, aiming to capture profitable price movements.

Dynamic RSI Integration: The RSI indicator helps refine entry signals by avoiding overbought situations.

User-Defined Parameters: Allows customization of exit thresholds and backtesting periods to suit individual trading preferences.

Commission and Slippage: The script factors in realistic commission fees (0.1%) and slippage (2%) for a more accurate backtesting experience.

Beats Buy-and-Hold: Backtesting suggests this strategy outperforms a simple buy-and-hold approach in uptrending markets.

Overall, the DCA Strategy offers a valuable approach for traders seeking to capitalize on long opportunities in trending markets with the help of Heikin Ashi candles and RSI confirmation.

Ichimoku Clouds Strategy Long and ShortOverview:

The Ichimoku Clouds Strategy leverages the Ichimoku Kinko Hyo technique to offer traders a range of innovative features, enhancing market analysis and trading efficiency. This strategy is distinct in its combination of standard methodology and advanced customization, making it suitable for both novice and experienced traders.

Unique Features:

Enhanced Interpretation: The strategy introduces weak, neutral, and strong bullish/bearish signals, enabling detailed interpretation of the Ichimoku cloud and direct chart plotting.

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Dual Trading Modes: Long and Short modes are available, allowing alignment with market trends.

Flexible Risk Management: Offers three styles in each mode, combining fixed risk management with dynamic indicator states for versatile trade management.

Indicator Line Plotting: Enables plotting of Ichimoku indicator lines on the chart for visual decision-making support.

Methodology:

The strategy utilizes the standard Ichimoku Kinko Hyo model, interpreting indicator values with settings adjustable through a user-friendly menu. This approach is enhanced by TradingView's built-in strategy tester for customization and market selection.

Risk Management:

Our approach to risk management is dynamic and indicator-centric. With data from the last year, we focus on dynamic indicator states interpretations to mitigate manual setting causing human factor biases. Users still have the option to set a fixed stop loss and/or take profit per position using the corresponding parameters in settings, aligning with their risk tolerance.

Backtest Results:

Operating window: Date range of backtests is 2023.01.01 - 2024.01.04. It is chosen to let the strategy to close all opened positions.

Commission and Slippage: Includes a standard Binance commission of 0.1% and accounts for possible slippage over 5 ticks.

Maximum Single Position Loss: -6.29%

Maximum Single Profit: 22.32%

Net Profit: +10 901.95 USDT (+109.02%)

Total Trades: 119 (51.26% profitability)

Profit Factor: 1.775

Maximum Accumulated Loss: 4 185.37 USDT (-22.87%)

Average Profit per Trade: 91.67 USDT (+0.7%)

Average Trade Duration: 56 hours

These results are obtained with realistic parameters representing trading conditions observed at major exchanges such as Binance and with realistic trading portfolio usage parameters. Backtest is calculated using deep backtest option in TradingView built-in strategy tester

How to Use:

Add the script to favorites for easy access.

Apply to the desired chart and timeframe (optimal performance observed on the 1H chart, ForEx or cryptocurrency top-10 coins with quote asset USDT).

Configure settings using the dropdown choice list in the built-in menu.

Set up alerts to automate strategy positions through web hook with the text: {{strategy.order.alert_message}}

Disclaimer:

Educational and informational tool reflecting Skyrex commitment to informed trading. Past performance does not guarantee future results. Test strategies in a simulated environment before live implementation

Megabar Breakout (Range & Volume & RSI)Hey there,

This strategy is based on the idea that certain events lead to what are called Megabars. Megabars are bars that have a very large range and volume. I wanted to verify whether these bars indicate the start of a trend and whether one should follow the trend.

Summary of the Code:

The code is based on three indicators: the range of the bar, the volume of the bar, and the RSI. When certain values of these indicators are met, a Megabar is identified. The direction of the Megabar indicates the direction in which we should trade.

Why do I combine these indicators?

I want to identify special bars that have the potential to mark the beginning of a breakout. Therefore, a bar needs to exhibit high volume, have a large range (huge price movement), and we also use the Relative Strength Index (RSI) to assess potential momentum. Only if all three criteria are met within one candle, do we use this as an identifier for a megabar.

Explanation of Drawings on the Chart:

As you can see, there is a green background on my chart. The green background symbolizes the time when I'm entering a trade. Only if a Megabar happens during that time, I'm ready to enter a trade. The time is between 6 AM and 4 PM CET. It's just because I prefer that time. Also, the strategy draws an error every time a Megabar happens based on VOL and Range only (not on the RSI). That makes it pretty easy to go through your chart and check the biggest bars manually. You can activate or deactivate these settings via the input data of the strategy.

When Do We Enter a Trade?

We wait for a Megabar to happen during our trading session. If the Megabar is bullish, we open a LONG trade at the opening price of the next candle. If the Megabar is bearish, we open a SHORT trade at the opening price of the next candle.

Where Do We Put Our Take Profit & Stop Loss?

The default setting is TP = 40 Pips and SL = 30 Pips. In that case, we are always trading with a risk-reward ratio of 1.33 by default. You can easily change these settings via the input data of the strategy.

Strategy Results

The criteria for Megabars were chosen by me in a way that makes Megabars something special. They are not intended to occur too frequently, as the fundamental idea of this strategy would otherwise not hold. This results in only 37 closed trades within the last 12 months. If you change the criterias for a megabar to a milder one, you will create more Megabars and therefore more trades. It's up to you. I have adapted this strategy to the 30-minute chart of the EURUSD. In the evaluation, we consider a period of 12 months, which I believe is sufficient.

My default settings for the indicators look like this:

Avg Length Vol 20

Avg Multiplier Vol 3

Avg Length Range 20

Avg Multiplier Range 4

Value SMA RSI for Long Trades 50

Value SMA RSI for Short Trades 70

IMPORTANT: The current performance overview does not display the results of these settings. Please change the settings to my default ones so that you can see how I use this strategy.

I do not recommend trading this strategy without further testing. The script is meant to reflect a basic idea and be used as a tool to identify Megabars. I have made this strategy completely public so that it can be further developed. One can take this framework and test it on different timeframes and different markets.

SILVER Midnight Candle Color Strategy 1-Hour Delay and SL/TP Overview:

The "Midnight Candle Color Strategy with 1-Hour Delay and SL/TP" is a unique trading strategy designed for the Forex market. This strategy capitalizes on the color of the midnight candle based on New York time, making trade decisions one hour later, at 1:00 AM.

Key Features:

Time Zone Adjustment: Automatically adjusts to New York time (UTC-5 or UTC-4 during Daylight Saving Time).

Midnight Candle Analysis: Utilizes the color of the midnight candle to gauge market sentiment.

Trade Execution at 1 AM: Trades are executed one hour after midnight based on the previous day's candle color.

Strategic SL/TP: Incorporates predefined stop loss (SL) and take profit (TP) levels for each trade.

How It Works:

The script first determines whether the current bar represents 12:00 AM or 1:00 AM in New York time.

At midnight, it records the color of the candle (green for bullish, red for bearish).

At 1:00 AM, the strategy:

Enters a long position if the midnight candle was green, with specific TP and SL settings.

Enters a short position if the midnight candle was red, again with defined TP and SL.

Visualization:

Optional markers are plotted on the chart for easy visualization of the strategy's entry points at midnight and 1 AM.

Usage Tips:

Ideal for traders focusing on overnight price movements and early morning trends.

Best suited for SILVER trading due to the 24-hour trading cycle.

We recommend backtesting the strategy with historical data to evaluate performance.

Disclaimer:

This strategy is provided for educational purposes and should not be considered as financial advice. Users should conduct their own research and exercise caution while trading. Past performance is not indicative of future results.

I´m not a signal service, however I´m sharing my signals. For free. If you wish to buy something, contact some other signalist, preferably with 5-10-15-20K followers, selling signals on the premium channel, but in reality not trading them themselves. If you will realise after few blown account that something is wrong, ask yourself why is that. Trading is not pushing the buy-sell button and drinking tequila on the beach. If you want to learn, you know what to do.

Liquidity Breakout - Strategy [presentTrading]- Introduction and How It Is Different

The Liquidity Breakout Strategy is a unique trading strategy that focuses on identifying and leveraging patterns in market price data. This strategy, mainly inspired by the script "Master Pattern" by LuxAlgo, takes a different approach from many traditional strategies that rely on technical indicators or fundamental analysis. Instead, the Liquidity Breakout is based on the concept of contraction detection and liquidity levels. This approach allows traders to identify potential trading opportunities that other strategies might miss.

BTCUSDT 6h

The strategy is different from other trading strategies because it uses a unique combination of pattern detection, liquidity levels, and user-defined trading direction. This combination allows the strategy to adapt to various market conditions and trading styles, making it a versatile tool for traders.

- Strategy: How It Works

1. Contraction Detection: The strategy uses a lookback period defined by the user (default is 10 bars) to identify contractions in the market. A contraction is a period where the market is consolidating, often followed by a significant price movement. The strategy identifies contractions by finding pivot highs and pivot lows within the lookback period. If a pivot high is lower than the previous pivot high and a pivot low is higher than the previous pivot low, a contraction is detected.

2. liquidity Levels:

What are Liquidity levels? Liquidity levels, also known as liquidity pools or zones, are price levels at which there is a significant amount of trading activity. They are often areas where large institutional traders (like banks or hedge funds) have placed orders. These levels are important because they can act as support or resistance levels, and price often reacts at these levels.

In the context of this strategy, liquidity levels are used to identify potential entry and exit points for trades. When the price reaches a liquidity level, it could indicate a potential trading opportunity. For example, if the price breaks through a liquidity level, it could signal the start of a new trend. On the other hand, if the price approaches a liquidity level and then reverses, it could signal a potential reversal.

The strategy uses these two elements to identify potential trading opportunities. When a contraction is detected, the strategy will look for a breakout in the direction of the trend. If the breakout occurs at a liquidity level, the strategy will execute a trade.

The strategy also allows traders to set their stop loss based on either the Average True Range (ATR) or a fixed percentage. This flexibility allows traders to manage their risk according to their personal risk tolerance and trading style.

- Trade Direction

One of the unique features of the Master Pattern Strategy is the ability to choose the trading direction. Traders can choose to trade in the "Long" direction, the "Short" direction, or "Both". This feature allows traders to adapt the strategy to their personal trading style and market outlook.

For example, if a trader believes that the market is in an uptrend, they can choose to trade only in the "Long" direction. Conversely, if the market is in a downtrend, they can choose to trade only in the "Short" direction. If the trader believes that the market is volatile and there are opportunities in both directions, they can choose to trade in "Both" directions.

- Usage

To use the strategy, traders need to input their preferred settings, including the contraction detection lookback period, liquidity levels, stop loss type, and trading direction. Once these settings are input, the strategy will automatically detect potential trading opportunities and execute trades according to the defined parameters.

- Default Settings

The default settings for the Master Pattern Strategy are as follows:

Contraction Detection Lookback: 10

Liquidity Levels: 20

Stop Loss Type: ATR

ATR Length: 20

ATR Multiplier: 3.0

Fixed Percentage: 0.01

Trading Direction: Both

These settings can be adjusted according to the trader's personal preferences and market conditions. It's recommended that traders experiment with different settings to find the ones that work best for their trading style and goals.

CCI+EMA Strategy with Percentage or ATR TP/SL [Alifer]This is a momentum strategy based on the Commodity Channel Index (CCI), with the aim of entering long trades in oversold conditions and short trades in overbought conditions.

Optionally, you can enable an Exponential Moving Average (EMA) to only allow trading in the direction of the larger trend. Please note that the strategy will not plot the EMA. If you want, for visual confirmation, you can add to the chart an Exponential Moving Average as a second indicator, with the same settings used in the strategy’s built-in EMA.

The strategy also allows you to set internal Stop Loss and Take Profit levels, with the option to choose between Percentage-based TP/SL or ATR-based TP/SL.

The strategy can be adapted to multiple assets and timeframes:

Pick an asset and a timeframe

Zoom back as far as possible to identify meaningful positive and negative peaks of the CCI

Set Overbought and Oversold at a rough average of the peaks you identified

Adjust TP/SL according to your risk management strategy

Like the strategy? Give it a boost!

Have any questions? Leave a comment or drop me a message.

CAUTIONARY WARNING

Please note that this is a complex trading strategy that involves several inputs and conditions. Before using it in live trading, it is highly recommended to thoroughly test it on historical data and use risk management techniques to safeguard your capital. After backtesting, it's also highly recommended to perform a first live test with a small amount. Additionally, it's essential to have a good understanding of the strategy's behavior and potential risks. Only risk what you can afford to lose .

USED INDICATORS

1 — COMMODITY CHANNEL INDEX (CCI)

The Commodity Channel Index (CCI) is a technical analysis indicator used to measure the momentum of an asset. It was developed by Donald Lambert and first published in Commodities magazine (now Futures) in 1980. Despite its name, the CCI can be used in any market and is not just for commodities. The CCI compares current price to average price over a specific time period. The indicator fluctuates above or below zero, moving into positive or negative territory. While most values, approximately 75%, fall between -100 and +100, about 25% of the values fall outside this range, indicating a lot of weakness or strength in the price movement.

The CCI was originally developed to spot long-term trend changes but has been adapted by traders for use on all markets or timeframes. Trading with multiple timeframes provides more buy or sell signals for active traders. Traders often use the CCI on the longer-term chart to establish the dominant trend and on the shorter-term chart to isolate pullbacks and generate trade signals.

CCI is calculated with the following formula:

(Typical Price - Simple Moving Average) / (0.015 x Mean Deviation)

Some trading strategies based on CCI can produce multiple false signals or losing trades when conditions turn choppy. Implementing a stop-loss strategy can help cap risk, and testing the CCI strategy for profitability on your market and timeframe is a worthy first step before initiating trades.

2 — AVERAGE TRUE RANGE (ATR)

The Average True Range (ATR) is a technical analysis indicator that measures market volatility by calculating the average range of price movements in a financial asset over a specific period of time. The ATR was developed by J. Welles Wilder Jr. and introduced in his book “New Concepts in Technical Trading Systems” in 1978.

The ATR is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The ATR can be used to set stop-loss orders. One way to use ATR for stop-loss orders is to multiply the ATR by a factor (such as 2 or 3) and subtract it from the entry price for long positions or add it to the entry price for short positions. This can help traders set stop-loss orders that are more adaptive to market volatility.

3 — EXPONENTIAL MOVING AVERAGE (EMA)

The Exponential Moving Average (EMA) is a type of moving average (MA) that places a greater weight and significance on the most recent data points.

The EMA is calculated by taking the average of the true range over a specified period. The true range is the greatest of the following:

The difference between the current high and the current low.

The difference between the previous close and the current high.

The difference between the previous close and the current low.

The EMA can be used by traders to produce buy and sell signals based on crossovers and divergences from the historical average. Traders often use several different EMA lengths, such as 10-day, 50-day, and 200-day moving averages.

The formula for calculating EMA is as follows:

Compute the Simple Moving Average (SMA).

Calculate the multiplier for weighting the EMA.

Calculate the current EMA using the following formula:

EMA = Closing price x multiplier + EMA (previous day) x (1-multiplier)

STRATEGY EXPLANATION

1 — INPUTS AND PARAMETERS

The strategy uses the Commodity Channel Index (CCI) with additional options for an Exponential Moving Average (EMA), Take Profit (TP) and Stop Loss (SL).

length : The period length for the CCI calculation.

overbought : The overbought level for the CCI. When CCI crosses above this level, it may signal a potential short entry.

oversold : The oversold level for the CCI. When CCI crosses below this level, it may signal a potential long entry.

useEMA : A boolean input to enable or disable the use of Exponential Moving Average (EMA) as a filter for long and short entries.

emaLength : The period length for the EMA if it is used.

2 — CCI CALCULATION

The CCI indicator is calculated using the following formula:

(src - ma) / (0.015 * ta.dev(src, length))

src is the typical price (average of high, low, and close) and ma is the Simple Moving Average (SMA) of src over the specified length.

3 — EMA CALCULATION

If the useEMA option is enabled, an EMA is calculated with the given emaLength .

4 — TAKE PROFIT AND STOP LOSS METHODS

The strategy offers two methods for TP and SL calculations: percentage-based and ATR-based.

tpSlMethod_percentage : A boolean input to choose the percentage-based method.

tpSlMethod_atr : A boolean input to choose the ATR-based method.

5 — PERCENTAGE-BASED TP AND SL

If tpSlMethod_percentage is chosen, the strategy calculates the TP and SL levels based on a percentage of the average entry price.

tp_percentage : The percentage value for Take Profit.

sl_percentage : The percentage value for Stop Loss.

6 — ATR-BASED TP AND SL

If tpSlMethod_atr is chosen, the strategy calculates the TP and SL levels based on Average True Range (ATR).

atrLength : The period length for the ATR calculation.

atrMultiplier : A multiplier applied to the ATR to set the SL level.

riskRewardRatio : The risk-reward ratio used to calculate the TP level.

7 — ENTRY CONDITIONS

The strategy defines two conditions for entering long and short positions based on CCI and, optionally, EMA.

Long Entry: CCI crosses below the oversold level, and if useEMA is enabled, the closing price should be above the EMA.

Short Entry: CCI crosses above the overbought level, and if useEMA is enabled, the closing price should be below the EMA.

8 — TP AND SL LEVELS

The strategy calculates the TP and SL levels based on the chosen method and updates them dynamically.

For the percentage-based method, the TP and SL levels are calculated as a percentage of the average entry price.

For the ATR-based method, the TP and SL levels are calculated using the ATR value and the specified multipliers.

9 — EXIT CONDITIONS

The strategy defines exit conditions for both long and short positions.

If there is a long position, it will be closed either at TP or SL levels based on the chosen method.

If there is a short position, it will be closed either at TP or SL levels based on the chosen method.

Additionally, positions will be closed if CCI crosses back above oversold in long positions or below overbought in short positions.

10 — PLOTTING

The script plots the CCI line along with overbought and oversold levels as horizontal lines.

The CCI line is colored red when above the overbought level, green when below the oversold level, and white otherwise.

The shaded region between the overbought and oversold levels is plotted as well.

SuperTrend Enhanced Pivot Reversal - Strategy [PresentTrading]

- Introduction and How it is Different

The SuperTrend Enhanced Pivot Reversal is a unique approach to trading that combines the best of two worlds: the precision of pivot reversal points and the trend-following power of the SuperTrend indicator. This strategy is designed to provide traders with clear entry and exit points, while also filtering out potentially false signals using the SuperTrend indicator.

BTCUSDT 6hr

ETHBTC 6hr

Unlike traditional pivot reversal strategies, this approach uses the SuperTrend indicator as a filter. This means that it only takes trades that align with the overall trend, as determined by the SuperTrend indicator. This can help to reduce the number of false signals and improve the overall profitability of the strategy.

The Pivot Reversal Strategy with SuperTrend Filter is particularly well-suited to the cryptocurrency market for the reason of High Volatility. This means that prices can change rapidly in a very short time, making it possible to make a profit quickly. The strategy's use of pivot points allows traders to take advantage of these rapid price changes by identifying potential reversal points

- Strategy: How it Works

The strategy works by identifying pivot reversal points, which are points in the price chart where the price is likely to reverse. These points are identified using a combination of the ta.pivothigh and ta.pivotlow functions, which find the highest and lowest points in the price chart over a certain period.

Once a pivot reversal point is identified, the strategy checks the direction of the SuperTrend indicator. If the SuperTrend is positive (indicating an uptrend), the strategy will only take long trades. If the SuperTrend is negative (indicating a downtrend), the strategy will only take short trades.

The strategy also includes a stop loss level, which is set as a percentage of the entry price. This helps to limit potential losses if the price moves in the opposite direction to the trade.

- Trade Direction

The trade direction can be set to "Long", "Short", or "Both". This allows the trader to choose whether they want to take only long trades (buying low and selling high), only short trades (selling high and buying low), or both. This can be useful depending on the trader's view of the market and their risk tolerance.

- Usage

To use the Pivot Reversal Strategy with SuperTrend Filter, simply input the desired parameters into the script and apply it to the price chart of the asset you wish to trade. The strategy will then identify potential trade entry and exit points, which will be displayed on the price chart.

- Default Settings

The default settings for the strategy are as follows:

ATR Length: 5

Factor: 2.618

Trade Direction: Both

Stop Loss Level: 20%

Commission: 0.1%

Slippage: 1

Currency: USD

Each trade: 10% of account equity

Initial capital: $10,000

These settings can be adjusted to suit the trader's preferences and risk tolerance. Always remember to test any changes to the settings using historical data before applying them to live trades.

Bollinger Bands Modified (Stormer)This strategy is based and shown by trader and investor Alexandre Wolwacz "Stormer".

Overview

The strategy uses two indicators Bollinger Bands and EMA (optional for EMA).

Calculates Bollinger Bands, EMA, highest high, and lowest low values based on the input parameters, evaluating the conditions to determine potential long and short entry signals.

The conditions include checks for crossovers and crossunders of the price with the upper and lower Bollinger Bands, as well as the position of the price relative to the EMA.

The script also incorporates the option to add an inside bar pattern check for additional information.

Entry Position

Long Position:

Price cross over the superior band of bollinger bands.

The EMA is used to add support for trend analysis, it is an optional input, when used, it checks if price is above EMA.

Short Position:

Price cross under the inferior band of bollinger bands.

The EMA is used to add support for trend analysis, it is an optional input, when used, it checks if price is under EMA.

Risk Management

Stop Loss:

The stop loss is calculated based on the input highest high (for short position) and lowest low (for long position).

It gets the length based on the input from the last candles to set which is the highest high and which is the lowest low.

Take Profit:

According to the author, the profit target should be at least 1:1.6 the risk, so to have the strategy mathematically positive.

The profit target is configured input, can be increased or decreased.

It calculates the take profit based on the price of the stop loss with the profit target input.

ATR GOD Strategy by TradeSmart (PineConnector-compatible)This is a highly-customizable trading strategy made by TradeSmart, focusing mainly on ATR-based indicators and filters. The strategy is mainly intended for trading forex , and has been optimized using the Deep Backtest feature on the 2018.01.01 - 2023.06.01 interval on the EUR/USD (FXCM) 15M chart, with a Slippage value of 3, and a Commission set to 0.00004 USD per contract. The strategy is also made compatible with PineConnector , to provide an easy option to automate the strategy using a connection to MetaTrader. See tooltips for details on how to set up the bot, and check out our website for a detailed guide with images on how to automate the strategy.

The strategy was implemented using the following logic:

Entry strategy:

A total of 4 Supertrend values can be used to determine the entry logic. There is option to set up all 4 Supertrend parameters individually, as well as their potential to be used as an entry signal/or a trend filter. Long/Short entry signals will be determined based on the selected potential Supertrend entry signals, and filtered based on them being in an uptrend/downtrend (also available for setup). Please use the provided tooltips for each setup to see every detail.

Exit strategy:

4 different types of Stop Losses are available: ATR-based/Candle Low/High Based/Percentage Based/Pip Based. Additionally, Force exiting can also be applied, where there is option to set up 4 custom sessions, and exits will happen after the session has closed.

Parameters of every indicator used in the strategy can be tuned in the strategy settings as follows:

Plot settings:

Plot Signals: true by default, Show all Long and Short signals on the signal candle

Plot SL/TP lines: false by default, Checking this option will result in the TP and SL lines to be plotted on the chart.

Supertrend 1-4:

All the parameters of the Supertrends can be set up here, as well as their individual role in the entry logic.

Exit Strategy:

ATR Based Stop Loss: true by default

ATR Length (of the SL): 100 by default

ATR Smoothing (of the SL): RMA/SMMA by default

Candle Low/High Based Stop Loss: false by default, recent lowest or highest point (depending on long/short position) will be used to calculate stop loss value. Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Candle Lookback (of the SL): 50 by default

Percentage Based Stop Loss: false by default, Set the stop loss to current price - % of current price (long) or price + % of current price (short).

Percentage (of the SL): 0.3 by default

Pip Based Stop Loss: Set the stop loss to current price - x pips (long) or price + x pips (short). Set 'Base Risk Multiplier' to 1 if you would like to use the calculated value as is. Setting it to a different value will count as an additional multiplier.

Pip (of the SL): 10 by default

Base Risk Multiplier: 4.5 by default, the stop loss will be placed at this risk level (meaning in case of ATR SL that the ATR value will be multiplied by this factor and the SL will be placed that value away from the entry level)

Risk to Reward Ratio: 1.5 by default, the take profit level will be placed such as this Risk/Reward ratio is met

Force Exiting:

4 total Force exit on custom session close options: none applied by default. If enabled, trades will close automatically after the set session is closed (on next candle's open).

Base Setups:

Allow Long Entries: true by default

Allow Short Entries: true by default

Order Size: 10 by default

Order Type: Capital Percentage by default, allows adjustment on how the position size is calculated: Cash: only the set cash amount will be used for each trade Contract(s): the adjusted number of contracts will be used for each trade Capital Percentage: a % of the current available capital will be used for each trade

ATR Limiter:

Use ATR Limiter: true by default, Only enter into any position (long/short) if ATR value is higher than the Low Boundary and lower than the High Boundary.

ATR Limiter Length: 50 by default

ATR Limiter Smoothing: RMA/SMMA by default

High Boundary: 1000 by default

Low Boundary: 0.0003 by default

MA based calculation: ATR value under MA by default, If not Unspecified, an MA is calculated with the ATR value as source. Only enter into position (long/short) if ATR value is higher/lower than the MA.

MA Type: RMA/SMMA by default

MA Length: 400 by default

Waddah Attar Filter:

Explosion/Deadzone relation: Not specified by default, Explosion over Deadzone: trades will only happen if the explosion line is over the deadzone line; Explosion under Deadzone: trades will only happen if the explosion line is under the deadzone line; Not specified: the opening of trades will not be based on the relation between the explosion and deadzone lines.

Limit trades based on trends: Not specified by default, Strong Trends: only enter long if the WA bar is colored green (there is an uptrend and the current bar is higher then the previous); only enter short if the WA bar is colored red (there is a downtrend and the current bar is higher then the previous); Soft Trends: only enter long if the WA bar is colored lime (there is an uptrend and the current bar is lower then the previous); only enter short if the WA bar is colored orange (there is a downtrend and the current bar is lower then the previous); All Trends: only enter long if the WA bar is colored green or lime (there is an uptrend); only enter short if the WA bar is colored red or orange (there is a downtrend); Not specified: the color of the WA bar (trend) is not relevant when considering entries.

WA bar value: Not specified by default, Over Explosion and Deadzone: only enter trades when the WA bar value is over the Explosion and Deadzone lines; Not specified: the relation between the explosion/deadzone lines to the value of the WA bar will not be used to filter opening trades.

Sensitivity: 150 by default

Fast MA Type: SMA by default

Fast MA Length: 10 by default

Slow MA Type: SMA

Slow MA Length: 20 by default

Channel MA Type: EMA by default

BB Channel Length: 20 by default

BB Stdev Multiplier: 2 by default

Trend Filter:

Use long trend filter 1: false by default, Only enter long if price is above Long MA.

Show long trend filter 1: false by default, Plot the selected MA on the chart.

TF1 - MA Type: EMA by default

TF1 - MA Length: 120 by default

TF1 - MA Source: close by default

Use short trend filter 1: false by default, Only enter long if price is above Long MA.

Show short trend filter 1: false by default, Plot the selected MA on the chart.

TF2 - MA Type: EMA by default

TF2 - MA Length: 120 by default

TF2 - MA Source: close by default

Volume Filter:

Only enter trades where volume is higher then the volume-based MA: true by default, a set type of MA will be calculated with the volume as source, and set length

MA Type: RMA/SMMA by default

MA Length: 200 by default

Date Range Limiter:

Limit Between Dates: false by default

Start Date: Jan 01 2023 00:00:00 by default

End Date: Jun 24 2023 00:00:00 by default

Session Limiter:

Show session plots: false by default, show market sessions on chart: Sidney (red), Tokyo (orange), London (yellow), New York (green)

Use session limiter: false by default, if enabled, trades will only happen in the ticked sessions below.

Sidney session: false by default, session between: 15:00 - 00:00 (EST)

Tokyo session: false by default, session between: 19:00 - 04:00 (EST)

London session: false by default, session between: 03:00 - 11:00 (EST)

New York session: false by default, session between: 08:00 - 17:00 (EST)

Trading Time:

Limit Trading Time: true by default, tick this together with the options below to enable limiting based on day and time

Valid Trading Days Global: 123567 by default, if the Limit Trading Time is on, trades will only happen on days that are present in this field. If any of the not global Valid Trading Days is used, this field will be neglected. Values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) To trade on all days use: 123457

(1) Valid Trading Days: false, 123456 by default, values represent days: Sunday (1), Monday (2), ..., Friday (6), Saturday(7) The script will trade on days that are present in this field. Please make sure that this field and also (1) Valid Trading Hours Between is checked

(1) Valid Trading Hours Between: false, 1800-2000 by default, hours between which the trades can happen. The time is always in the exchange's timezone

All other options are also disabled by default

PineConnector Automation:

Use PineConnector Automation: false by default, In order for the connection to MetaTrader to work, you will need do perform prerequisite steps, you can follow our full guide at our website, or refer to the official PineConnector Documentation. To set up PineConnector Automation on the TradingView side, you will need to do the following:

1. Fill out the License ID field with your PineConnector License ID;

2. Fill out the Risk (trading volume) with the desired volume to be traded in each trade (the meaning of this value depends on the EA settings in Metatrader. Follow the detailed guide for additional information);

3. After filling out the fields, you need to enable the 'Use PineConnector Automation' option (check the box in the strategy settings);

4. Check if the chart has updated and you can see the appropriate order comments on your chart;

5. Create an alert with the strategy selected as Condition, and the Message as {{strategy.order.comment}} (should be there by default);

6. Enable the Webhook URL in the Notifications section, set it as the official PineConnector webhook address and enjoy your connection with MetaTrader.

License ID: 60123456789 by default

Risk (trading volume): 1 by default

NOTE! Fine-tuning/re-optimization is highly recommended when using other asset/timeframe combinations.

Grid Spot Trading Algorithm V2 - The Quant ScienceGrid Spot Trading Algorithm V2 is the last grid trading algorithm made by our developer team.

Grid Spot Trading Algorithm V2 is a fixed 10-level grid trading algorithm. The grid is divided into an accumulation area (red) and a selling area (green).

In the accumulation area, the algorithm will place new buy orders, selling the long positions on the top of the grid.

BUYING AND SELLING LOGIC

The algorithm places up to 5 limit orders on the accumulation section of the grid, each time the price cross through the middle grid. Each single order uses 20% of the equity.

Positions are closed at the top of the grid by default, with the algorithm closing all orders at the first sell level. The exit level can be adjusted using the user interface, from the first level up to the fifth level above.

CONFIGURING THE ALGORITHM

1) Add it to the chart: Add the script to the current chart that you want to analyze.

2) Select the top of the grid: Confirm a price level with the mouse on which to fix the top of the grid.

3) Select the bottom of the grid: Confirm a price level with the mouse on which to fix the bottom of the grid.

4) Wait for the automatic creation of the grid.

USING THE ALGORITHM

Once the grid configuration process is completed, the algorithm will generate automatic backtesting.

You can add a stop loss that destroys the grid by setting the destruction price and activating the feature from the user interface. When the stop loss is activated, you can view it on the chart.

BankNifty 5min Supertrend Based StrategyBankNifty 5min Supertrend Based Strategy, Intraday.

Work Best at 5mint chart on BankNifty.

The strategy is designed to trade using the Supertrend indicator with session-based rules, and risk management. It allows for customization through input variables and aims to provide a clear visual representation of the Supertrend by changing the color .

The script also includes input variables for the trading session and date range, which allows the trader to specify the time period in which they want the strategy to run. The session variable specifies the start and end times of the trading session, which in this case is set to the Indian trading session from 9:15 am to 3:10 pm.

The strategy starts by defining input variables such as the session time, start and end date for the backtesting, the length of the ATR, and the Supertrend factor. It also includes options for delay at session start and stop loss points and trail percentage .

The code then checks if the current time is within the specified session and date range . If it is, the Supertrend and its direction are calculated using the defined input variables. The strategy then waits for N numbers of candles (defined by the User) to form at the start of every session i.e. 09:15 AM before entering a trade.

The entry and exit conditions for long and short trades are defined based on the change in the Supertrend direction and the number of candles formed at the session start i.e. 09:15 AM . After that, it takes entry and exit for long and short trades on the change in the Supertrend direction . Stop-loss and trailing stop-loss are also defined based on the input variables.

Stop-loss (Defined by the user) is fixed points either below or above the Entry Price for Long and Short entries.

The Supertrend plot is displayed with changing colors depending on the direction. Finally, the strategy closes all trades at the end of the session if there are any open trades.

Overall, this strategy aims to trade with the Supertrend indicator using session-based rules and risk management.

However, as with any trading strategy, it is important to thoroughly test it before using it in live trading .

DRM StrategyOne of the ways I go when I develop strategies is by reducing the number of parameters and removing fixed parameters and levels.

In this strategy, I'm trying to create an RSI indicator with a dynamic length.

Length is computed based on the correlation between Price and its momentum.

You can set min and max values for the RSI, and if the correlation is close to 1, we'll be at a min RSI value. When it's -1, we'll be at the max level.

I got this idea from Sofien Kaabar's book.

The strategy is super simple, and there might be much room for improvement.

Performance on the deep backtesting is not excellent, so I think the strategy needs some filters for regimes, etc.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.